As documents go, sinking fund forecasts aren’t that too hard to read, but they are packed full of information about the running of a body corporate scheme that’s easy to overlook.

A typical sinking fund forecast starts with some general information about the purpose of the report and the nature of the building, including its age, the number of lots and the unit entitlements. There will also be a line item showing the balance of the fund at the time the report was written, and this figure, combined with the condition of your building, will strongly influence the recommendations that follow.

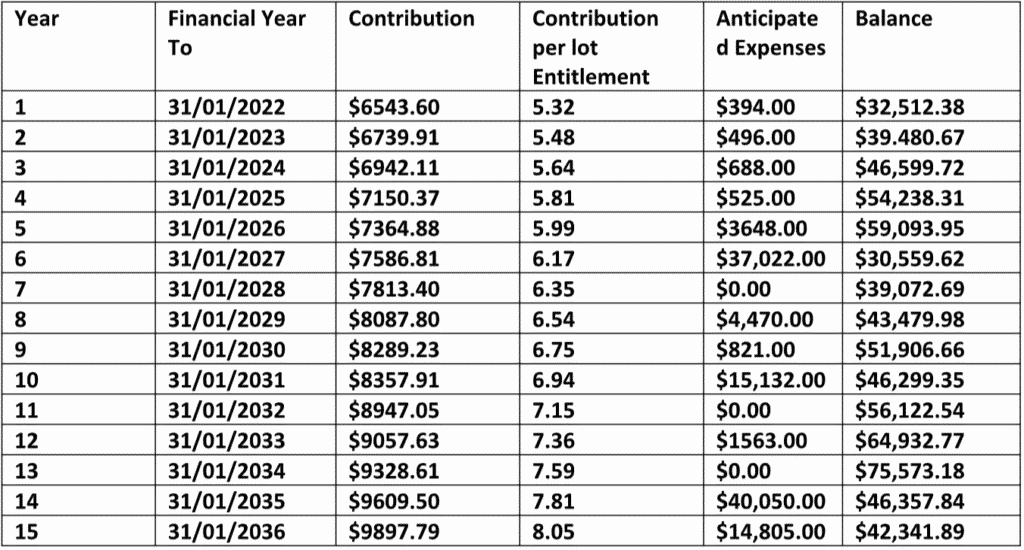

The meat of the forecast comes in the recommended contributions over a 15-year period. Depending on the company you have used to provide your report, the terminology and presentation of this information will vary, but typically you will see a table or some tables that detail proposed annual contributions and spending while setting out the anticipated position of the plan at the end of each period. They may look something like the table below, although this is a condensed version for ease of use.

What information does the Sinking Fund Forecast contain?

Let’s unpack some of that information contained within the Sinking Fund Forecast:

Year/Financial Year to

‘Financial Year To’ is the year of the sinking fund forecast from the date of creation, while the financial year is the financial year of the plan in which the expected contribution should be made.

Contribution

‘Contribution’: tells you how much you should budget for as a sinking fund contribution in that financial year. In the example shown in the above table, the anticipation is that in the financial year to 31/01/2022, the scheme should budget $6543.60. Typically, this is the number that a body corporate manager will list when providing you with a budget proposal for your site as they rely on the forecast for budgeting purposes.

Contribution per Lot Entitlement

‘Contribution per lot entitlement’: tells you how much each unit entitlement will pay as a part of the recommended contribution. It can be a difficult one for people to interpret as owners don’t always think about their unit in terms of entitlements. If you are discussing the sinking fund forecast, it may be beneficial to multiply this figure out so that an actual dollar figure of contribution per lot per annum can be seen. It’s much easier for someone to understand that they need to contribute $960 per annum to the sinking fund than it is for them to know they will pay $7.92 per lot entitlement per annum.

Anticipated Expenses

‘Anticipated Expenses’: These are expenses expected from the sinking fund on a year to year basis. Later in the document, these will be detailed with a breakdown of all expenses. It’s worth noting that while the recommended contributions are usually kept fairly steady with small increases over time to help owners with financial planning, the anticipated expenses can fluctuate significantly on a year to year basis. This reflects the fact that while there may be some quiet years when owners make minimal investments in a scheme, these are likely to be followed by years when a major project is undertaken.

Many people tend to think of the sinking fund as just being for savings, but it is really a guide for spending and the savings are raised to facilitate that.

Balance

‘Balance’: this is the anticipated balance at the end of the financial year. Figures include additional anticipated income from interest via term deposits.

That’s the headline information but the remainder of the document contains some key small print in the anticipated expense and exclusions that can be easy to overlook.

The anticipated expenditures section usually sets out in detailed tables a multitude of standard maintenance items, how much they might cost to repair and when the repair might be anticipated. An individual line item may look something like this:

Here, the reports anticipate an expenditure of $1947.00 on downpipe repairs in 2025 and a further $4332.00 in 2028.

How much faith should you place in the Sinking Fund Forecast?

The obvious question is how much faith should you place in these projections? Well, no one has a crystal ball so the figures aren’t an absolute directive.

If your gutters are in good working order in 2027 when the report is predicting repairs are required, there’s no need to take any action. Equally, the gutters may have had problems earlier than average, and you might have had to pay for them in 2024. Most sinking fund forecasts have some contingency budgeting to allow for this unforeseen expenditure, but otherwise, they will consider the balance of probabilities in their projections and owners will have to be practical in their interpretations of how to undertake expenditure.

This allows some scope for owners to defer payments and works which is why many schemes don’t follow the sinking fund forecasts, but over the long run costs like this often balance themselves out. The gutters may not need work in 2027 but perhaps the intercom system breaks down that same year a couple of years before it should. Schemes that follow the contributions schedule tend to have the capacity to ride these situations out. Those that don’t can find the problems quickly mounting up.

So, What’s NOT Included in the Sinking Fund Forecast?

Just as important as what is included in the report is what is not. Along with checking the expected costs, you need to review the exclusions as there can be some large cost items that aren’t considered.

Safety items aren’t in there. Nor, usually, is fire maintenance or expenses for lifts. Items that are usually covered in the admin budget, such as maintaining the gardens or air conditioners, are not part of the report. Upgrades, as opposed to maintenance, also aren’t there, so if you want to substantially improve your pool, additional funding may have to be sought. Forewarned is forearmed so even if your scheme followed a forecast to the letter you could still reasonably expect further costs over time.

This post appears in Strata News #471.

William Marquand Tower Body Corporate E: willmarquand@towerbodycorporate.com.au P: 07 5609 4924